What is a Contract for Difference?

Definition

In the energy sector, a Contract for Difference (CfD) is a subsidy model for renewable energy. Under this model, the plant operator receives subsidies when market conditions result in particularly low revenue, but must also repay funds when high electricity prices lead to particularly high revenue. The idea behind this is that investors are guaranteed a minimum payment per kilowatt-hour generated, while revenues are capped to conserve funding. A two-way CfD is often referred to as a symmetric market premium.

At the end of 2026, the European Union’s state aid approval for Germany’s current renewable energy support system will expire. To date, plants have been subsidized with a sliding-scale market premium that guarantees operators a minimum return. According to EU regulations, by 2027 at the latest, electricity-price-linked subsidies must be replaced by Contracts for Difference (CfDs) or comparable schemes.

For this reason, the federal government is currently drafting an amendment to the Renewable Energy Sources Act (EEG). On the one hand, the changes are intended to maintain incentives for the expansion of renewable energy. On the other hand, they are intended to permanently prevent so-called windfall profits, such as those that occurred due to exorbitantly high electricity prices during the 2022/2023 energy crisis. The EU views CfDs as a way to promote renewable energy while simultaneously recouping revenue from plant operators whose earnings exceed a fixed cap. When market prices are high, the government can generate revenue through the cap and use it for the public good. At the same time, CfDs offer plant operators a high degree of investment security through a minimum payment (“floor”).

How does a Contract for Difference work?

The following CfD models could be used by the government to skim off profits. As yet, there is no preferred model for Germany.

Hourly CfD

With the hourly CfD model, plant operators receive a subsidy if the hourly reference price is below the applicable value. If, on the other hand, the hourly reference price is above the applicable value, plant operators must repay the difference between the applicable value and the reference price. The applicable value is typically determined through a bidding process and remains constant for the duration of the subsidy.

The reference price is determined using the following methods for calculating market value:

- Reference price = hourly day-ahead market price: The reference price for hourly CfDs corresponds, for each of the 24 hours of each day, to the respective volume-weighted average price for electricity from all generation types on the day-ahead market.

- Reference price = technology-specific hourly day-ahead market price: In this case, the reference price is calculated as the generation- and volume-weighted average of the hourly prices for a specific technology (e.g., PV or wind power).

The use of the generation-weighted average takes into account the fact that, for example, volatile energy sources such as wind and PV do not feed into the grid at a constant rate at all times. The technology-specific market value more accurately reflects when and how much was fed into the grid and thus more precisely mirrors the prices actually achieved on the day-ahead market.

More to read

Monthly CfD

The monthly CfD model works similarly to the hourly model, with the difference that the time frame changes from one hour to one month. The reference price is calculated as follows:

- Reference price = monthly market price: The reference price is calculated as the volume-weighted average of all day-ahead prices for a given month, regardless of technology.

- Reference price = technology-specific monthly market price: The technology-specific monthly market price is calculated as the generation- and volume-weighted average of the monthly prices for a specific technology (e.g., PV or wind power).

The following also applies to this model: If the reference price exceeds the applicable value, plant operators are required to repay the difference. If, on the other hand, the applicable value is lower, they receive a subsidy, also equal to the difference between the applicable value and the reference price.

Annual CfD

Similar to the two CfD models mentioned above, the two reference prices are also calculated for this model, but based on annual market prices:

- Reference price = annual market price: The annual market price is calculated as the volume-weighted average of all day-ahead prices for the year in question, regardless of the technology.

- Reference price = technology-specific annual market price: The reference price corresponds to the generation- and volume-weighted average of the annual prices for a specific technology (e.g., PV or wind power).

Plant operators are paid the difference per kWh fed into the grid if the annual reference price is below the applicable value. However, if the annual reference price is higher, they are required to pay the difference per kWh fed into the grid to the government.

A CfD therefore significantly reduces a plant’s exposure to market prices. The actual revenue from an asset deviates from the target value only to the extent that the actual revenues from direct sales under a CfD regime differ from the average revenue of the respective generation type.

Revenue structure of a plant with a CfD:

Spot market revenues + (Target value - Average revenue for the generation type) <-> Target value + (Spot market revenues - Average revenue for the generation type)

As weather conditions are the decisive factor for the feed-in profile of renewable energy plants, the revenues of plants within a given generation type are very similar. The potential for additional revenues is therefore limited, especially since the subsidy conditions only allow for certain types of marketing. CfDs on a cap-and-floor basis promise greater market exposure.

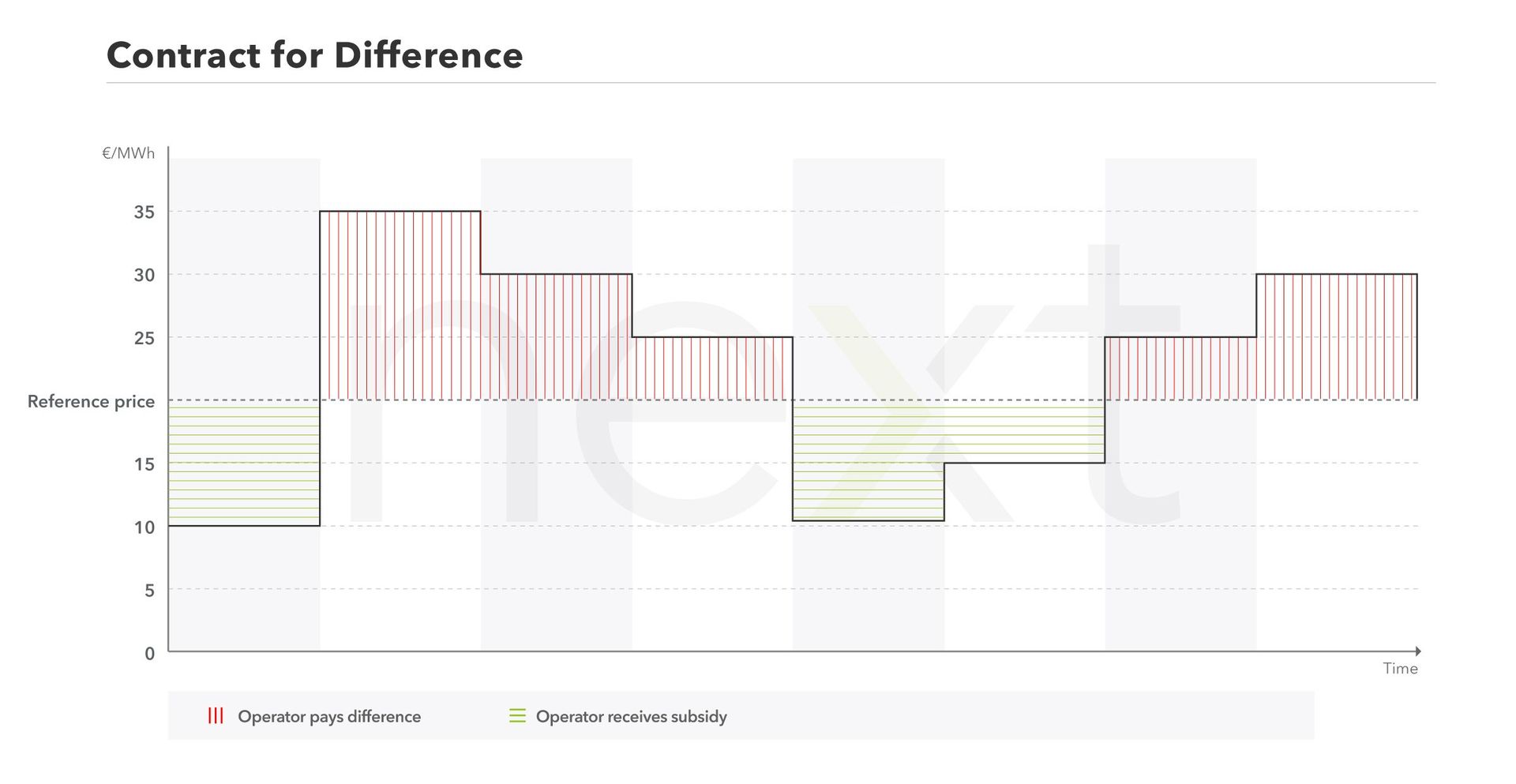

Cap-and-Floor CfD

The cap-and-floor-based CfD is characterized by a range within which plant operators can generate market-based revenues. This range is bounded by the “floor” as the lower limit and the “cap” as the upper limit. Within this market value range, the operator receives no subsidies and is not required to make any payments to the government. If the market value rises above the cap within a defined period (e.g., a day, month, or year), repayments to the government are due. If, on the other hand, the market value falls below the floor, the operator receives a subsidy. Market exposure is also limited, but significantly higher than in a CfD with only a single reference value.

When it comes to tenders, there are various options for determining the cap and floor:

- Fixed corridor width: The width of the price corridor (e.g., 20 EUR/MWh) is specified, and bids are submitted at the midpoint. Alternatively, the floor is bid, and a fixed corridor width is added to it.

- Percentage revenue cap: In the call for bids, the cap is specified as a percentage that is added to the floor to be bid.

- Fixed revenue cap: The cap is set before the call for bids; bidders specify the floor in their bids.

Der Februar 2026 geleakte Arbeitsstand des Gesetzentwurfs lässt durchblicken, dass die Bundesregierung eine Cap-and-Floor-Lösung bevorzugt.

How do CfDs compare to the market premium?

Support through a sliding market premium, as previously applied in Germany, guarantees operators a minimum revenue per kilowatt-hour fed into the grid. This “reference value” was determined at auctions in which bidders submitted their bids in ct/kWh. The lowest bids were awarded the contract.

If, later during operation, the average revenues for the respective generation type (PV, onshore wind, offshore wind) fell below the winning bid price, operators received the difference as a subsidy. If the average revenues were higher, no subsidy was paid. However, plant operators were allowed to keep all revenues generated. Until 2022, the subsidy was refinanced through the so-called EEG surcharge, which was added to the price of electricity. Since 2023, it has been paid for out of tax revenue.

Even with a CfD, plant operators receive subsidies if their average revenues fall below the benchmark value. In return, however, they are required to repay funds if their average revenues exceed the benchmark value. Since this approach pools not only shortfalls but also surpluses, it is also referred to as a symmetric market premium.

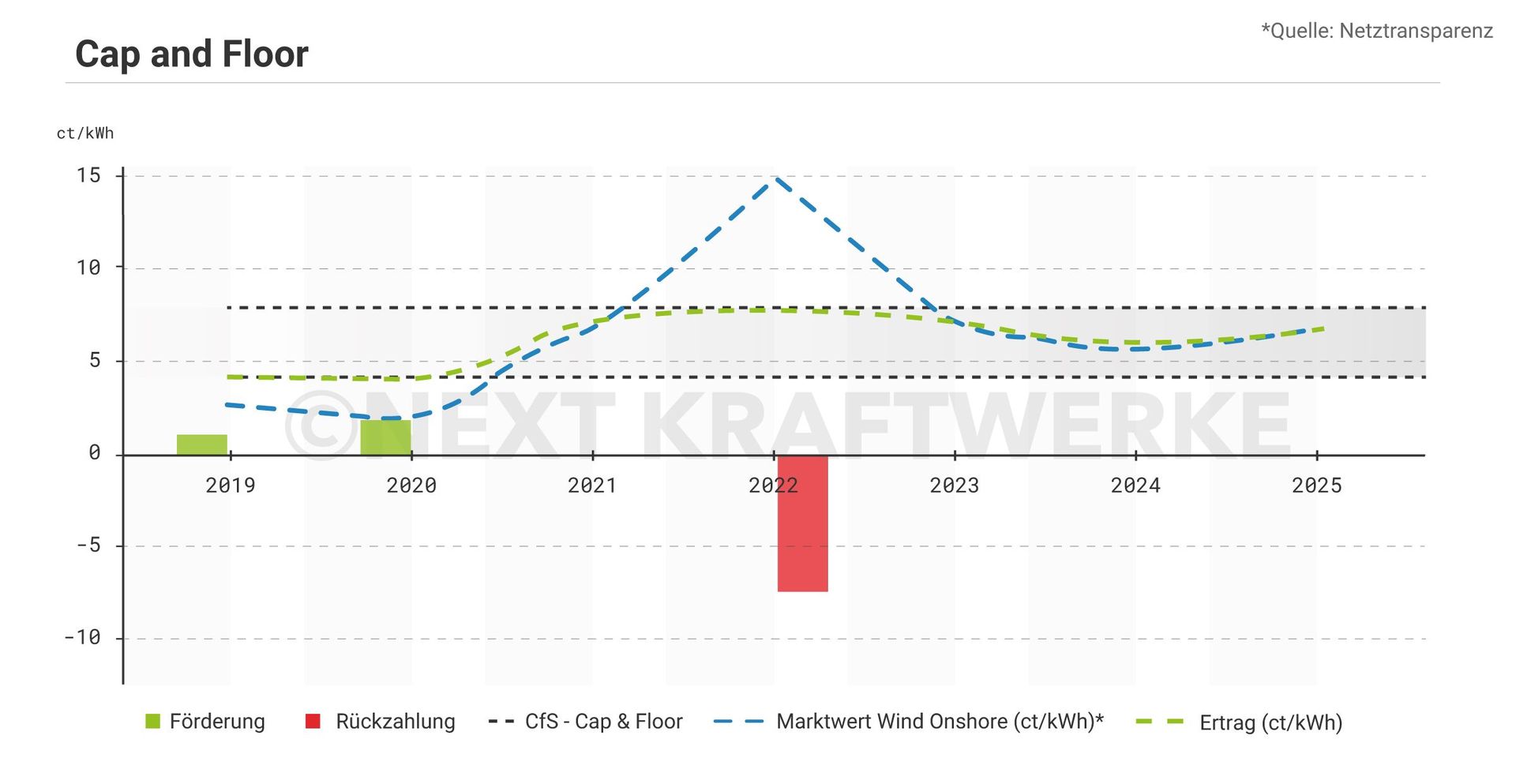

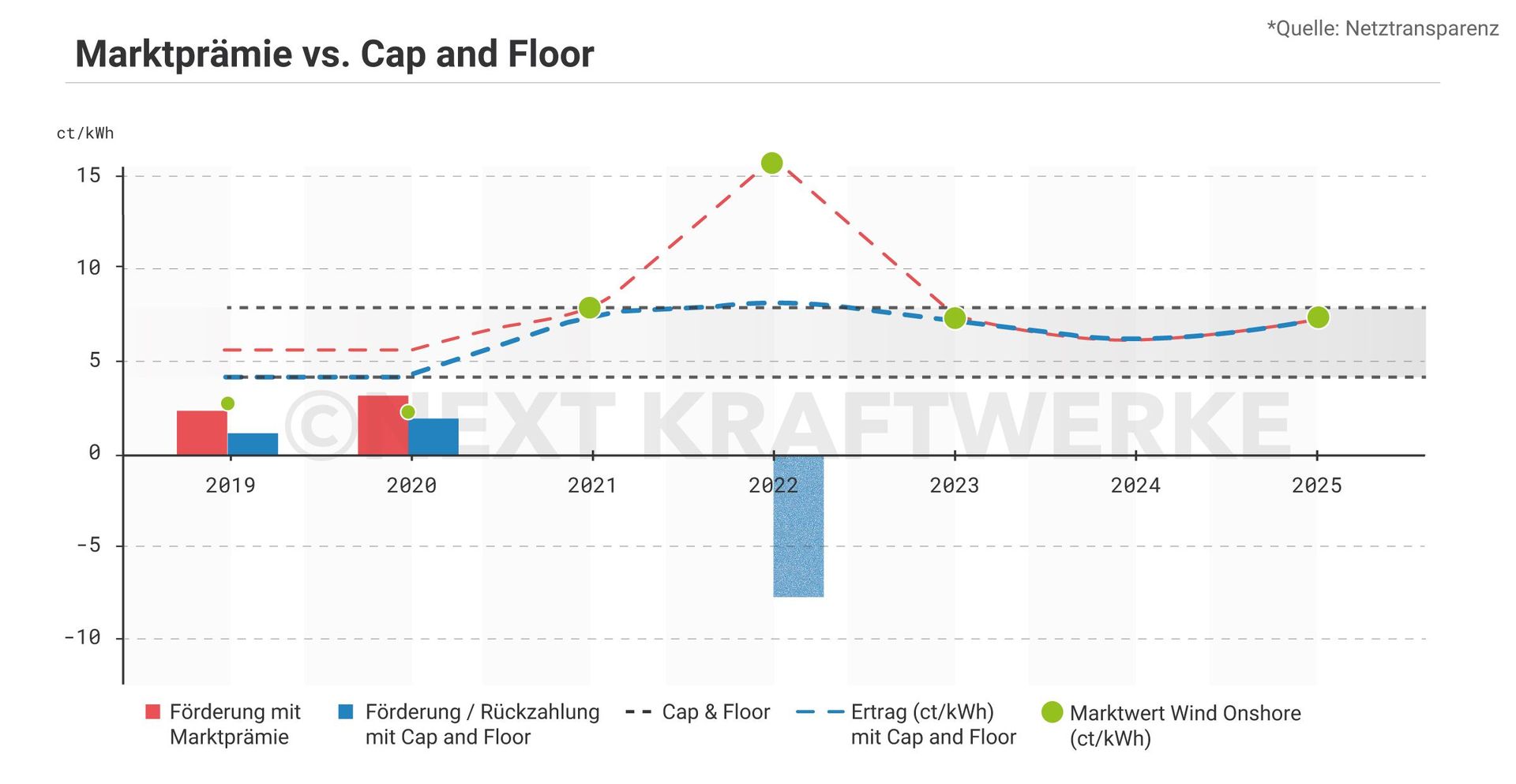

(The following chart show how the different subsidy types would have affected the subsidies and revenues of an average onshore wind turbine from 2020 to 2025.)

Legal Situation: What role do CfDs currently play in promoting renewable energy in Germany?

The possibility of supporting wind and solar power through CfDs rather than a sliding-scale market premium was already being discussed before the first EEG in 2014. However, as long as the revenues regularly fell below the feed-in tariffs, this remained largely an internal industry debate. It only gained traction among the broader public when, in the wake of the energy crisis, operators’ revenues exceeded the feed-in tariffs many times over.

Despite warnings from the EU, the German federal government once again secured a special exemption from Brussels for the 2023 EEG amendment in order to be allowed to continue the market premium subsidy scheme. Starting in 2027, under European law, new support mechanisms must include bilateral CfDs or comparable mechanisms, at least if the support is to remain tied to physical feed-in.

The following are considered alternatives:

- Linking subsidies to theoretical feed-in volumes that would have been possible with the respective technology under given weather conditions.

- A capacity market in which plant operators are compensated solely for maintaining generation capacity, regardless of how much they actually feed into the grid. However, these are considered unsuitable for renewable energy sources, as the call on their capacity is weather-dependent.

In both cases, revenue from the sale of the generated electricity would be added. However, the German government’s working paper, which was leaked in February, explicitly mentions Contracts for Difference.

What economic advantages and disadvantages are attributed to CFDs?

Contracts for Difference are generally considered fairer because, under the floating market premium, the public hedges against the risk of low electricity prices but does not share in the proceeds when electricity prices are high. However, there are also concerns that capped revenues could have undesirable side effects. Industry representatives such as the German Renewable Energy Federation (BEE), for example, emphasize that rigid CfDs could distort price signals in the electricity market and slow down the energy transition, while a cap-and-floor model could represent a sensible solution to meet EU requirements. Here are some key arguments in the debate.

Investment Incentives

Proponents believe that CfDs create a stable investment climate that lowers the cost of capital and thereby encourages investment. As the share of renewable energy continues to rise, power plants could “cannibalize” each other due to weather-dependent feed-in capabilities: If all plants can feed power into the grid at the same time, the price of electricity drops, often even below zero. This risk would be covered by CfDs.

Critics warn, however, that capping revenues could slow the expansion of wind and solar facilities because it would leave little room for economic opportunities. In the medium term, according to economic analysis, this would result in only moderate profit opportunities. A cap-and-floor CfD could therefore be a middle ground.

Flexibility and Grid-Supportive Behavior

Support through a CfD does not meet the requirement to promote flexibility and grid-supportive power generation from renewable energy plants: If the high revenues generated by feeding power into the grid during electricity shortages do not remain with the companies, there is no incentive for such grid-supportive power generation.

Higher Electricity Prices

Critics fear that CfD support could fail to achieve its most important goal: reducing the burden on the general public. The argument is that bids from plant operators in future auctions would be higher. In some market premium auctions, bids as low as 0 cents have been successful. This means that these plants receive subsidies only if their average annual revenue falls below zero. The reasoning is that revenue from periods of high electricity prices is sufficient to make the investment worthwhile. However, if revenue from high-price periods is lost because these periods trigger repayments, operators are once again reliant on subsidies to operate their plants profitably, and would consequently submit higher bids.

Are there already CfD subsidies in other countries?

The EU has been calling for subsidy models similar to CfDs for several years now. The United Kingdom serves as the benchmark model in this regard; it was still a member of the EU when it introduced renewable energy subsidies through CfDs in 2014 and made them its sole subsidy model in 2017.

France gradually introduced the “supplementary payment” (“complément de rémunération”) starting in 2015. This mechanism is similar to CfD remuneration but includes two restrictions: First, no premium is paid for electricity fed into the grid during periods of negative electricity prices; second, generators are only required to repay premiums they have received, thereby ruling out negative subsidies.

Ireland first auctioned off subsidies for wind turbines using bilateral contracts for difference in 2020. Spain, Poland, Denmark, and other countries followed suit starting in 2021.

Note: Next Kraftwerke assumes no liability for the completeness, accuracy, or timeliness of the information provided. This article is for informational purposes only and does not constitute individual legal advice.